Easy methods to Construct Imply Reversion Methods in Currencies

Our article explores a easy imply reversion buying and selling technique utilized to FX futures, specializing in figuring out undervalued and overvalued currencies to generate returns. Utilizing FX futures somewhat than spot charges permits for the inclusion of rate of interest differentials, simplifying the evaluation. The technique employs two position-sizing strategies—linear and exponential—each rebalanced month-to-month primarily based on forex deviations from their imply. Whereas the linear technique gives stability, its returns are restricted. In distinction, the exponential technique, regardless of larger danger and deeper drawdowns, in the end delivers stronger development and higher general efficiency by leveraging the imply reversion tendencies of FX pairs.

Introduction

Imply reversion is a basic idea in monetary markets that implies asset costs and returns ultimately transfer again towards their historic common or imply degree over time. This phenomenon could be noticed throughout varied asset courses, together with equities, commodities, and currencies – notably in forex pairs inside FX markets. As an alternative of solely specializing in spot alternate charges, it’s typically extra helpful to make use of FX futures for analyses. The rationale for that is that FX futures steady information collection incorporate the rate of interest differentials between currencies, routinely together with the carry return. If we rely solely on spot charges, corresponding to EUR/USD, we would wish to manually calculate and regulate for swap factors to account for the prices or advantages of holding a higher-yielding forex towards a lower-yielding one.

By analyzing a basket of currencies, we are able to calculate a median alternate fee and determine which currencies have deviated considerably from this imply. People who transfer too removed from the imply tend to revert, creating a chance to purchase undervalued currencies and brief overvalued ones, which is consistent with the pure mean-reverting tendency of FX pairs.

Thus, we arrived on the speculation: if we assemble a easy technique that goes lengthy on undervalued currencies and brief on overvalued ones, we are going to generate extra returns that exceed common anticipated returns, no matter market actions or the benchmark. In different phrases, we purpose to attain pure alpha efficiency.

Technique evaluation

For this technique, we used each day adjusted costs of FX futures traded on derivatives exchanges, particularly AD1 (futures on the Australian Greenback), BF1 (futures on the British Pound), CD1 (futures on the Canadian Greenback), EC1 (futures on the Euro), SF1 (futures on the Swiss Franc) and JY1 (futures on the Japanese Yen). We’re utilizing the continual futures for our evaluation. Extra particulars on methods to construct such information collection could be present in our older publish, Steady Futures Contracts Methodology for Backtesting. The dataset covers the interval from February 13, 2007 to September 5, 2024, throughout which solely the final accessible value of every month was chosen for the next analyses.

In step one, we calculated the cumulative return of every FX future on the final buying and selling day of the month and created an “common futures” collection, that’s used over the course of the evaluation as an anchor in direction of which the all particular person steady FX futures are likely to imply revert.

If a person FX future exceeded the common (it’s an overvalued forex), we went brief; in any other case, if it was under the common (it’s an undervalued forex), we went lengthy. This strategy is just like a grid buying and selling technique, which is described in additional element in research corresponding to What’s the Relation Between Grid Buying and selling and Delta Hedging? or A Primer on Grid Buying and selling Technique. Because the FX futures contracts are signed for a particular interval, we take care of them when it comes to constantly rolled futures information collection. To take care of our positions even after they expire, we promote them earlier than the expiration date and purchase new ones. Thus, we guarantee their ongoing holding.

After all, a very powerful query for any imply reverting technique is to methods to assign weights for particular person currencies. We determined to set weights such that the bigger the distinction between the given particular person steady futures information collection and the common, the better the load assigned to the brief/lengthy place. There are two doable methods for managing this – linear or exponential. In each circumstances, we repeated this course of month-to-month.

Linear place sizing

In linear place sizing, we used the distinction between the given steady futures collection and the common futures collection as the load for the brief/lengthy place. For instance, if the continual futures collection of a forex is 20% larger (20% decrease) than the common of all futures collection, then we go brief 20% of the forex (go 20% lengthy), and so forth.

Exponential place sizing

Within the exponential strategy, we additionally utilized the distinction between the person steady futures and the common information collection, however this time, the load for the brief/lengthy place is about within the exponential type. As an illustration, if the person steady future was 20% larger (20% decrease) than the common, we allotted 40% of the forex to a brief place (40% to a protracted place). If the person steady future was 30% larger (30% decrease) than the common, we allotted 90% of the forex to a brief place (90% to a protracted place), and so forth (160% weight for a 40% distinction, and many others.). After all, there’s a danger of uncontrolled leverage development when utilizing the exponential place sizing, but when utilized appropriately, it’s manageable and never overly harmful.

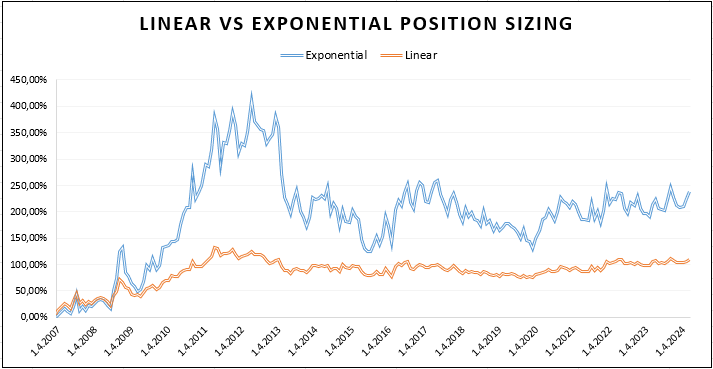

Comparability of the place sizing strategies

And the way do the overall weights of the portfolios managed by linear and exponential weightings develop over time? We will evaluation that by wanting on the image in Determine 2. As we are able to see, the overall weights of futures within the portfolio (complete leverage) can rise considerably within the intervals when particular person steady futures transfer far-off from the common, which serves because the anchor for the portfolio. In distinction, the linear place sizing is extra steady, and the overall place measurement hardly ever exceeds 150%; it often oscillates across the 100% worth.

Linear vs Exponential Imply Reversion Buying and selling Technique

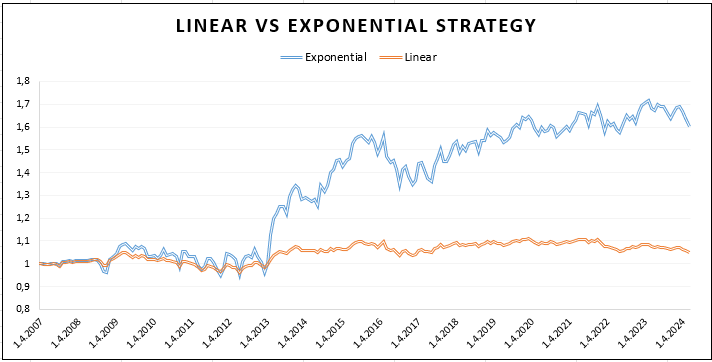

Based mostly on linear place sizing, we created a linear imply reversion buying and selling technique, and equally, an exponential imply reversion buying and selling technique was developed utilizing exponential place sizing. Each methods are rebalanced month-to-month, with FX futures chosen for brief or lengthy positions primarily based on the identical precept—shorting overvalued and shopping for the undervalued steady futures. The first distinction between the 2 methods lies within the weight invested in every FX future, which is set by linear or exponential place sizing. Each portfolios began with an preliminary worth of 1.

The linear technique proven in Determine 3 seems steady, with insignificant drawdowns however no tendency to develop. The worth of the linear technique portfolio has fluctuated round 1.1 for 10 years, which isn’t fascinating in any respect. This poor efficiency is additional confirmed by the low Sharpe ratio of 0.12 and the Calmar ratio of 0.05 (proven in Desk 1). Then again, the buying and selling technique with the exponential place sizing portfolio delivers engaging constructive extra returns (all returns are calculated from the continual futures information collection and, due to this fact, are extra returns over the money) with a Sharpe ratio of 0.35.

Conclusion

The imply reversion conduct is a well-utilizable characteristic in lots of fields of the investing world, and as we have now noticed, it additionally applies to forex FX futures. By leveraging this property, we are able to construct a worthwhile technique, notably together with the exponential place sizing technique. Nonetheless, nothing is free, and there’s a danger that its software might create uncontrollable leverage. Our exponential place sizing doesn’t have excessively excessive complete leverage (450% within the most level), so if sensible danger administration is used, the easy imply reversion methods in currencies can be utilized as a diversifier or supply of a further uncorrelated return within the broader multi-asset multi-strategy portfolio. After all, extra refined strategies for place sizing could be developed than the 2 we have now introduced. Nonetheless, our purpose was to point out the potential of the easy forex mean-reversion methods as a bunch and to not develop the absolute best buying and selling technique. We’ll depart the doable paths to enhance efficiency and return-to-risk ratios of mean-reverting methods for future articles.

Creator: Sona Beluska, Quant Analyst, Quantpedia.com

Are you searching for extra methods to examine? Join our e-newsletter or go to our Weblog or Screener.

Do you need to be taught extra about Quantpedia Premium service? Verify how Quantpedia works, our mission and Premium pricing supply.

Do you need to be taught extra about Quantpedia Professional service? Verify its description, watch movies, evaluation reporting capabilities and go to our pricing supply.

Are you searching for historic information or backtesting platforms? Verify our listing of Algo Buying and selling Reductions.

Or comply with us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookCheck with a good friend