Sundry Pictures

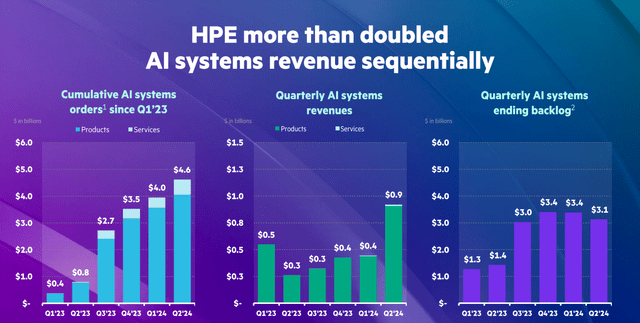

Hewlett Packard Enterprise (HPE) posted higher than anticipated Q2 FY24 earnings of $0.42 per share (non-GAAP) and income price $7.2bn, beating consensus estimates for $0.39 EPS and $6.83bn in revenues. The intense spot was actually the efficiency of the server phase, the place revenues rose by 18% y/y and 15% q/q after a stoop by 23% y/y in Q1. Particularly, the corporate reported a doubling of AI system revenues to $0.9bn from $0.4bn in Q1, which was the spotlight of the Q2 report.

The final time I advisable HPE was in Oct 2023 when the inventory traded $15 per share. My fundamental funding thesis again then was that it was a worth AI play, contemplating its low cost in comparison with friends. This time round, I put a robust purchase score on the inventory provided that the inventory has remained underappreciated in comparison with friends corresponding to Dell Applied sciences (DELL) and the worth proposition is even higher.

Server revenues lead the cost in Q2 as order conversion improves

For those who adopted carefully the Q1 earnings report, the earnings beat may not come as a shock, provided that the corporate missed forecasts within the earlier quarter attributable to issues with GPU availability that added to a major backlog of AI server orders. HPE stated in its newest earnings launch that it managed to exceed income forecasts due to stronger AI programs order conversion, suggesting a few of its earlier points with changing orders have been alleviated. Particularly, the cumulative orders for AI programs reached $4.6bn, up from $4.0bn in Q1 FY24. On the identical time, the backlog for AI programs declined by $3.1bn from $3.4bn in Q1 FY24. The advance so as conversion was additionally noticed in free money move, which rose to $610mn from $288mn in the identical quarter of 2023.

HPE earnings presentation Q2 FY24

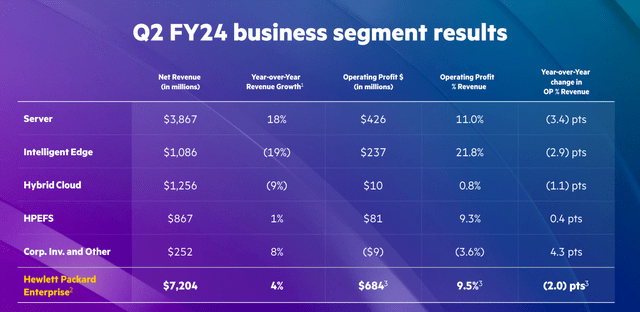

It ought to be famous that server revenues now embrace each revenues from high-performance computing and AI, in addition to the non-AI conventional server enterprise. Thus, the 18% y/y is all of the extra spectacular provided that the AI-led progress managed to offset the cyclical underperformance of conventional servers, which nonetheless stay a considerable portion of revenues.

Intelligence Edge revenues proceed to underperform, however might need bottomed

Revenues from the Clever Edge phase fell by 19% y/y as demand for networking options continued to melt attributable to a reversion to the imply after the very sturdy 2023 efficiency. Nonetheless, the phase seemingly noticed a trough in Q2 and can begin to recuperate within the second half of the 12 months, led by seasonal elements corresponding to demand from training establishments. The Clever Edge phase remained probably the most worthwhile for the corporate with 21.8% working revenue margin in comparison with 11.0% for the server phase and 9.5% for the complete firm in Q2, the corporate’s earnings report confirmed. Thus, the phase accounted for 37% of the whole revenue whereas producing solely 15.1% of the revenues.

The Clever Edge has complemented the server enterprise properly for HPE in current quarters, posting sturdy progress whereas the server enterprise was down. As well as, the phase has allowed the corporate to put up higher profitability than friends with an EBITDA margin of 17.8% over the previous 12 months in comparison with 9.89% for Dell (DELL), and 10.04% for Tremendous Micro Laptop (SMCI), that are two of the opposite large gamers within the AI server enterprise. Thus, regardless that the phase has weighed on income prior to now two quarters, it’s nonetheless a boon for profitability.

HPE earnings presentation Q2 FY24

HPE upgrades 2024 revenue steerage after Q2 earnings beat

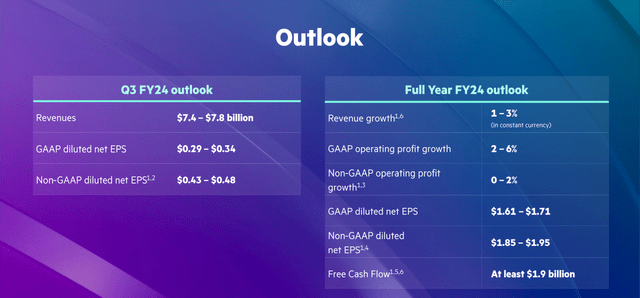

HPE barely upgraded the outlook for 2024 income progress to 1%-3% from 0%-2% beforehand anticipated in Q1. On the identical time, non-GAAP working revenue is estimated at 0%-2%, which is unchanged from the earlier estimate. HPE now anticipates non-GAAP EPS within the $1.85 to $1.95 vary, from $1.82-$1.92 beforehand anticipated. I feel these numbers stay somewhat conservative and HPE retains potential to proceed to shock on the upside in the remainder of 2024.

HPE earnings presentation Q2 FY24

Finest cause to personal HPE stays value

The very best cause to personal HPE stays its value, which continues to be at solely 9 occasions non-GAAP earnings over the previous 12 months. You’ll hardly discover higher worth within the tech sector for an organization that has publicity to AI. Compared, Dell continues to commerce at practically 19 occasions TTM earnings, whereas SMCI trades at round 40 occasions TTM earnings. Behind HPE’s comparatively low-cost valuation stays analysts’ conviction that the corporate will be unable to develop sooner or later and can stagnate. The consensus forecast for EPS progress over the following 3–5 years is 2.73%, in line with analysts polled by Looking for Alpha. If one assumes that the inventory will develop at a quicker tempo than GDP over the following 5 years, the inventory might be thought of undervalued.

I feel HPE ought to commerce at P/E multiples nearer to the place DELL is at present standing, contemplating its comparable publicity to the AI server enterprise, higher supercomputing experience and stronger positions in networking. I feel buyers will finally recognise that HPE is a well-run firm and the low cost is unjustified. Even when the corporate fails to ship on progress, HPE has a robust model title and is prone to stay in enterprise; therefore, draw back threat stays pretty low.

HPE stays uncovered to AI by way of totally different channels

One other necessary high quality for HPE is that it stays uncovered to the AI growth by way of totally different channels. The obvious ones stays the high-performance computing and AI phase, however Clever Edge and HPE Greenlake also can profit from AI. For example, edge computing can permit firms to carry out AI inferencing on the edge, doubtlessly permitting networking firms to seize a larger share of the AI pie.

As AI adoption strikes from large-scale information facilities the place AI coaching is completed to smaller firms with particular AI wants, I feel edge computing will finally see increased AI-fuelled progress. This places HPE in place to profit from the following wave of AI adoption. The acquisition of Juniper Networks for $14bn, which was introduced in January, will even enhance HPE’s means to ship AI inferencing on the edge.

The emergence of AI additionally makes information extra beneficial to retain, which basically improves prospects for HPE Greenlake hybrid storage. HPE is uniquely positioned to cowl AI wants from the sting, to hybrid cloud storage, to AI servers and supercomputers, which helps the corporate acquire purchasers. This may be seen from info shared by the corporate that a good portion of the AI programs orders are going by way of the HPE Greenlake platform.

Flattening of AI orders progress, falling margins elevate some issues

One of many damaging developments within the report was the flattening of cumulative AI programs orders which rose by $600mn in Q2 in comparison with $500mn in Q1 and $800mn in This autumn 2023. Thus, progress stays under ranges seen in 2023, regardless that the big backlog of orders will stay a robust tailwind for revenues within the coming quarters.

Then again, revenue margins considerably compressed in Q2 because the working revenue margin fell to 9.5% from 11.5% in Q2 2023 led by each the Clever Edge and Server segments. Nonetheless, I’m nonetheless not overly involved about this provided that HPE retains good profitability and dividend yield in comparison with friends as it’s rated A in each profitability and Dividend Yield in Looking for Alpha’s Sector Relative Grade.

Total, the primary issue that may decide value within the close to future is the corporate’s means to ship on progress. In that vein, the corporate’s comparatively low R&D funds and excessive dividend payout ratio might jeopardize its means to innovate and compete with rivals as competitors between AI gamers intensifies.

Conclusion

Valuing an organization like HPE stays very troublesome because it has chronically underperformed rivals prior to now 10 years since its inception and plenty of buyers stay on the side-lines. Nonetheless, I feel that AI adjustments the sport and can permit the corporate to develop at a a lot quicker tempo going ahead. The Q2 earnings rightfully show that the corporate can trip the AI wave efficiently. Finally, I imagine that HPE ought to slim at the least half of the valuation hole to DELL. Thus, I imagine {that a} 50% upside from the Jun 4 closing value of 17.6% is unquestionably attainable and my goal for the inventory is $25.