")

bjdlzx

Bonterra Vitality Corp. (OTCPK:BNEFF) reported outcomes that held up fairly nicely as a result of oil gross sales {dollars} now dominate the outcomes. If pure gasoline costs get well as anticipated, then this former pure gasoline producer will certainly profit. However the future is changing into extra and extra hooked up to grease. This continues the dialogue that started with the final article. The distinction is that now a pure gasoline pricing restoration seems to be a certainty within the close to future. That might give this firm extra cash to repay debt which might decrease the debt ratio. An preliminary dividend could also be within the intermediate future as nicely. The brand new administration is performing as anticipated and reporting a lot improved outcomes.

Second Quarter Highlights

Regardless of the sizable decline in pure gasoline costs (which up to now would have been a close to catastrophe for money movement) outcomes held up fairly nicely. This confirms that the administration technique of including liquids to manufacturing is a smart transfer.

(Observe That Bonterra Vitality is a Canadian Firm That Stories Utilizing Canadian {Dollars} Except In any other case Famous.)

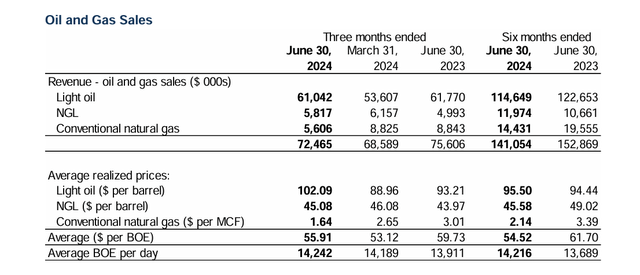

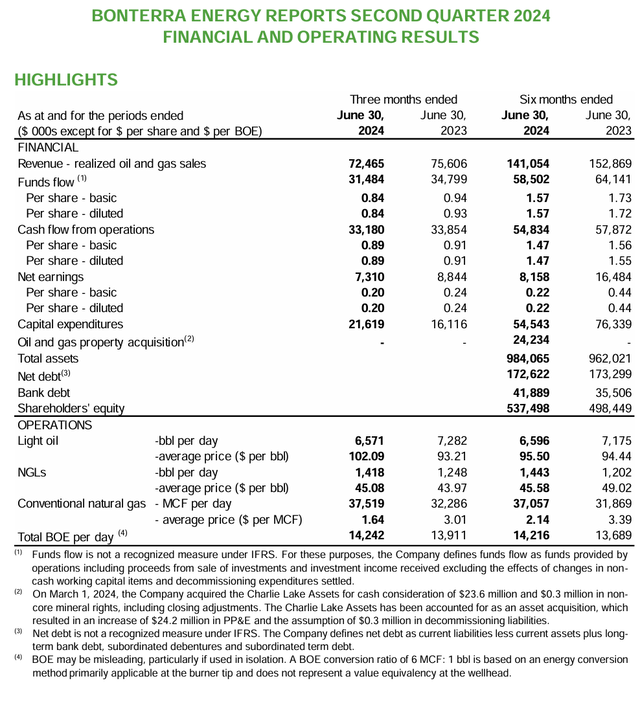

Bonterra Vitality Abstract Of Income Sources (Bonterra Vitality Second Quarter 2024, Outcomes Filed With Sedar)

Though oil itself is lower than half of the whole manufacturing, it’s now a lot of the gross sales {dollars}. Pure gasoline is now within the place of constructing the scenario higher, however now not doing the harm it did up to now when it was the main target of manufacturing. The most recent Charlie Lake acquisition will doubtless edge that manufacturing proportion of oil and liquids up a little bit extra to proceed the pattern of extra oil gross sales {dollars}.

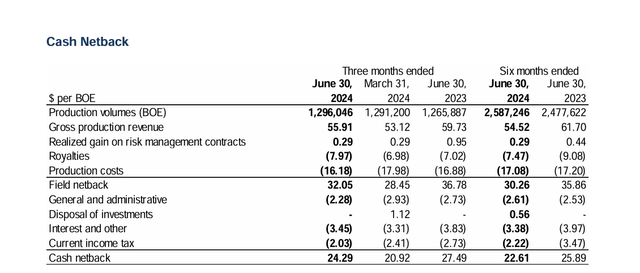

Bonterra Vitality Working Netback Comparability (Bonterra Vitality Second Quarter 2024, Outcomes Filed With Sedar)

The sphere netback and the money netback truly elevated over the primary quarter to comply with oil costs regardless of the weakening pure gasoline costs. The netback held up fairly nicely attributable to nonoperating causes like a decrease royalty price and a decrease earnings tax provision. On this enterprise, a little bit luck like that counts as a lot as working prowess.

As administration drills extra worthwhile wells, the sector netback ought to progressively change into a higher proportion of the manufacturing income to point out that the company breakeven might nicely drop. Some issues that ought to lower over time could be curiosity expense per barrel and (if manufacturing grows) common and administrative per barrel.

Ought to the corporate efficiently develop by acquisition, the method might velocity up.

Portfolio Decisions

The portfolio now has a greater variety of enticing selections that ought to allow the corporate to thrive below a number of completely different eventualities.

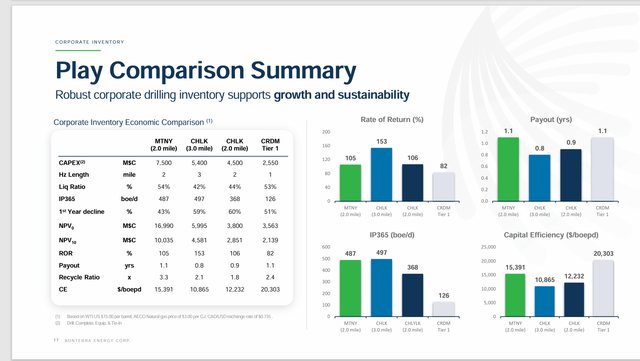

Bonterra Vitality Abstract Of Canadian Performs (Bonterra Vitality Second Quarter 2024, Company Presentation)

The pattern within the business in the direction of longer wells is clearly demonstrated right here. Charlie Lake’s 3-mile-long wells are probably the most worthwhile of the portfolio given present assumptions about costs.

Nevertheless, issues might shift considerably when pure gasoline costs start the anticipated restoration. North America is anticipated to realize plenty of export capability this 12 months and the following fiscal 12 months for pure gasoline. That will allow the continent to hitch the normally far stronger world pricing market. If that occurs, the connection between oil and gasoline pricing might change sufficient to make the profitability a little bit bit completely different.

Within the meantime, the corporate has some worthwhile selections that it by no means had earlier than whereas it waits to see if pure gasoline costs get well and the way lengthy that restoration lasts.

Return Of Capital Framework

The resurgence of money movement, even with extra debt has allowed this former income-modeled firm to start to speak about shareholder returns in all probability starting within the subsequent fiscal 12 months. After all, commodity costs have to cooperate a bit for that to occur. However the total administration assumptions appear to be cheap.

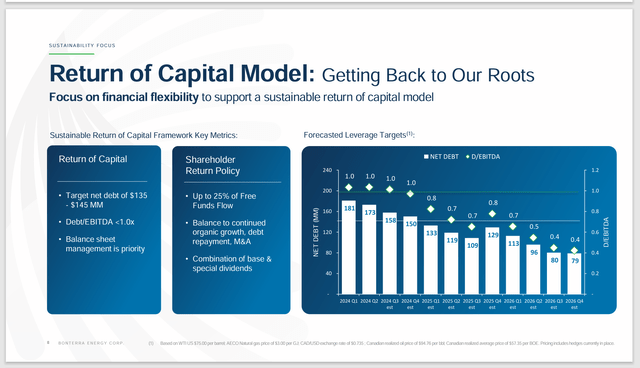

Bonterra Vitality Abstract Of Return Of Capital Steering (Bonterra Vitality Second Quarter 2024, Company Presentation)

Regardless of all of the acquisitions, the corporate has been capable of preserve the debt ratio cheap. That implies that shareholders can lastly take into consideration returns that was routine for this firm.

The distinction this time round is that the payout ratio goes to be so much decrease, and the corporate is more likely to proceed to accumulate acreage in locations like Charlie Lake sooner or later.

As was the case for a lot of corporations, the earnings mannequin didn’t work significantly nicely and left the corporate poorly positioned to face future challenges. New administration seems to have largely fastened the scenario. However the future is way extra more likely to be a progress and earnings mannequin with a defensible primary dividend. Then there’s flexibility to accommodate cyclical downturns.

The market is more likely to look ahead to a observe report below the “new regime” earlier than revaluing the inventory as funds have been squeezed for some time. However Canada has some very low-cost acquisition costs which enabled a fairly fast answer.

Earnings

Proper now, Charlie Lake is probably the most worthwhile a part of the portfolio. However don’t be stunned if the know-how that enabled 3-mile wells at Charlie Lake spreads to different areas as time strikes ahead. The result’s that earnings will doubtless proceed to show a drop within the company breakeven value.

Bonterra Vitality Abstract Of Monetary Outcomes Second Quarter 2024 (Bonterra Vitality Second Quarter 2024, Outcomes Filed With Sedar)

The necessary a part of the outcomes is that money movement is holding up unexpectedly nicely for these used to an organization that was extremely dependent upon pure gasoline. The attention-grabbing factor to notice is that regardless of the acquisition, the debt is roughly on the identical stage it was within the earlier fiscal 12 months. Therefore, manufacturing is a bit larger for a similar debt stage.

Whereas that manufacturing distinction is presently manufactured from decrease worth liquids and pure gasoline, the corporate is clearly going to be drilling for extra gentle oil manufacturing sooner or later.

A lot of the acquired acreage has been produced by utilizing older know-how that resulted in a much less worthwhile manufacturing combine. Nevertheless, that won’t be true of latest wells drilled.

Abstract

Administration had famous that a number of new wells had come on-line. This firm is sufficiently small that every nicely is probably going materials to the reported manufacturing combine. Nevertheless, on condition that new wells got here on-line and have been cleansing up, I’d count on that manufacturing combine to go in the direction of the next total proportion of sunshine oil and possibly some condensate within the manufacturing combine. Different liquids might climb as a proportion of manufacturing as nicely. Together with this might be a slight outperformance expectation that will result in a little bit manufacturing progress.

Charlie Lake is an rising play as a result of development of know-how that has allowed the play to change into very price aggressive with different established elements of the Canadian business.

The second quarter did have some upkeep and different points that influenced manufacturing as nicely. That is typical through the Spring Breakup in Canada.

This firm is a robust purchase consideration in that new administration has reinvigorated an organization that badly wanted a turnaround from an concept that was simply not working very nicely anymore. The consequence has been an organization with a sturdy manufacturing combine that ought to allow the corporate to thrive below numerous conditions. I’d additionally count on extra acquisitions sooner or later for this to change into a progress and earnings play.

Bonterra Vitality had repute amongst traders for fairly a while. It will seem that may once more change into the case sooner or later due to the efforts of the brand new administration.

Dangers

Any upstream firm is topic to the dangers of risky commodity costs which have extraordinarily low future visibility. A extreme and sustained downturn might change the outlook for the corporate.

Clearly, the brand new administration has been an element within the firm’s turnaround. A lack of providers of any of the brand new senior officers might have a fabric impact on firm prospects sooner or later.

The know-how advances that proceed to periodically sweep the business might make one other basin not within the portfolio (or interval) probably the most cost-effective within the business. That might require some portfolio changes by administration which present administration seems to have the ability to do. Nevertheless, there’s at all times some threat till the corporate “will get the place it must go”.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please pay attention to the dangers related to these shares.