Can We Use Energetic Share Measure as a Predictor?

Introduction

Energetic Share is a metric launched to quantify the diploma to which a portfolio differs from its benchmark index. It’s expressed as a proportion, starting from 0% (totally overlapping with the benchmark) to 100% (fully completely different). The idea gained reputation as a result of it was believed that larger Energetic Share displays really energetic administration, which may doubtlessly result in outperformance. If used accurately, Energetic Share may assist the buyers determine future winners, making it a doubtlessly efficient technique.

Nonetheless, in accordance with the paper Energetic Share and the Predictability of the Efficiency of Separate Accounts by Martijn Cremers, larger Energetic Share doesn’t constantly correlate with higher efficiency and reveals restricted potential to foretell the longer term success of energetic funds. Primarily based on these findings, the primary goal of this examine is to investigate this downside and discover whether or not the excessive Energetic Share funds are simply fairness issue (sensible beta) funds in disguise. Our speculation is that, in lots of instances, the fairness components influence funds’ efficiency and never the person portfolio managers’ idiosyncratic choices.

Knowledge

For this evaluation, we utilized each day information from 22 Energetic Share funds, sourced from the ActiveShare.information web site. One of many creators of this platform is Martijn Cremers, the writer of the aforementioned examine. A serious added worth of this web site is its dual-level benchmark analysis. It not solely examines the first benchmark designated by the portfolio supervisor of a given fund but additionally investigates the precise benchmark. It seeks to reduce Energetic Share by figuring out which benchmark higher aligns with the fund’s true funding technique than the one chosen by the portfolio supervisor. It’s common for portfolio managers to decide on benchmarks such because the S&P 500, though the fund’s identify and technique clearly point out a totally completely different funding universe (e.g., small-cap, mid-cap, or worth shares). Consequently, the fund ought to have a extra applicable benchmark precisely replicate its efficiency. This frequent mismatch is among the explanation why Energetic Share, whereas a preferred measure, typically lacks important explanatory energy in apply.

Our dataset of twenty-two Energetic Share funds, all of which used the S&P 500 chosen as their benchmark, was divided into 2 teams. The primary group encompass 11 Energetic Share funds with excessive Energetic Share relative to the chosen benchmark, although this benchmark was incorrectly chosen. In distinction, the second group contains 11 Energetic Share funds with excessive Energetic Share relative to a accurately chosen benchmark.

All out there info on ActiveShare.information relating to the Energetic Share of given funds is as of December 31, 2021. Our evaluation, nonetheless, is predicated on each day information from December 31, 2019, to December 31, 2023, sourced from Yahoo Finance. We think about this 4 yr interval sufficiently lengthy for statement and don’t anticipate important modifications within the Energetic Share of the funds, as this measure normally stays steady over time. However, a couple of funds didn’t exist for your entire interval, so their observations started later than these of the others.

Major evaluation

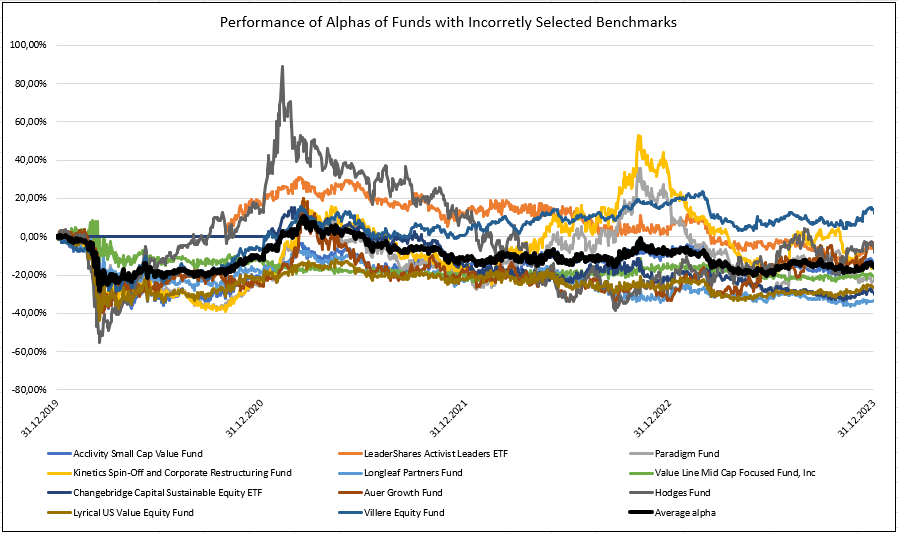

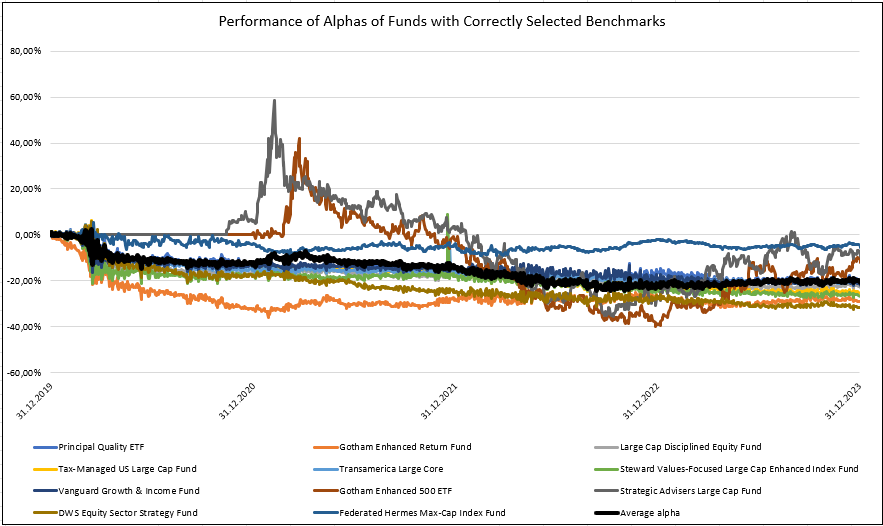

Firstly, for each teams of Energetic Share funds, we calculated the each day alpha relative to the benchmark chosen by the supervisor, on this case S&P 500, and in contrast it to the their common alpha.

As we are able to see from each photos, the typical fund underperforms the benchmark (SPY ETF—SPDR S&P 500 ETF Belief and the index ETF we picked). This isn’t stunning and is enough to the well-known proven fact that it’s onerous to systematically harvest alpha within the mutual fund area within the large-cap US shares funding universe.

Secondly, we calculated the each day adjusted costs of every fund, uploaded them into Quantpedia’s Portfolio Supervisor, and carried out an element evaluation, as described within the article How one can Replicate Any Portfolio. Afterwards, we carried out an Alpha Evaluation, the place every fund was decomposed into components to find out which portion of its alpha is attributed to residual alpha – representing the unexplainable a part of the fund, or the idiosyncratic danger of the supervisor, and which portion is attributable to artificial alpha, the a part of the alpha explainable by systematic components. Extra particulars about Alpha Evaluation process might be discovered within the article Quantpedia in November 2023.

Instance

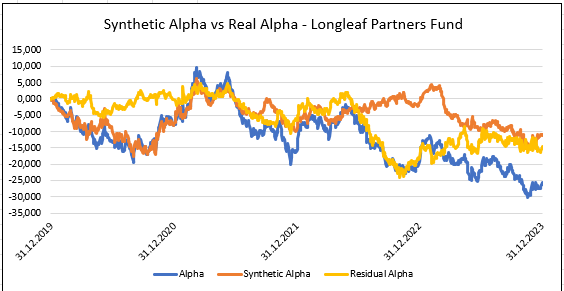

For example of outcomes achieved by performing these analyses on the examined Energetic Share funds, graphs associated to the Longleaf Companions Fund are offered beneath. The Longleaf Companions Fund makes use of the S&P 500 as its benchmark for Energetic Share (99% Energetic Share), although that is an incorrect alternative. Appropriate benchmark for this fund is the S&P 500 Pure Progress (98% Energetic Share).

Image 3 reveals the decomposition of the fund’s Alpha into the half that may be defined by systematic components – “Artificial Alpha” and the half that stems from the person idiosyncratic choices of the fund supervisor – “Residual Alpha“. What’s Image 3 telling us? On this case, up till mid-2022, many of the returns of the fund could possibly be defined by systematic components (the blue line could be very near the orange one). After that, the supervisor began to take idiosyncratic bets that didn’t repay (Residual Alpha, yellow line, plummeting along with fund Alpha in opposition to S&P 500, blue line). In 2023, fund underperformance continued collectively as a result of systematic components to which the fund was uncovered, and the fund ended up within the pattern with a destructive Alpha. Residual Alpha (idiosyncratic bets) and Artificial Alpha (systematic bets) contributed roughly the identical.

Within the image 4, we are able to evaluation the Alpha decomposition in a greater element a and we see, that systematic issue, which underperformed probably the most have been financials and the general US equities market issue (in the direction of which the fund was most likely slightly underweight). That systematic underperformance most likely displays the difficulty of the incorrectly chosen benchmark by the supervisor (benchmark different then S&P 500 needs to be picked by the supervisor).

Nonetheless, this evaluation was simply an instance of how alpha decomposition works on the person stage. We wish to see what it appears to be like like if we have now extra funds, and for that, we have to run alpha decomposition for all funds from our pattern and common out the numbers.

Outcomes

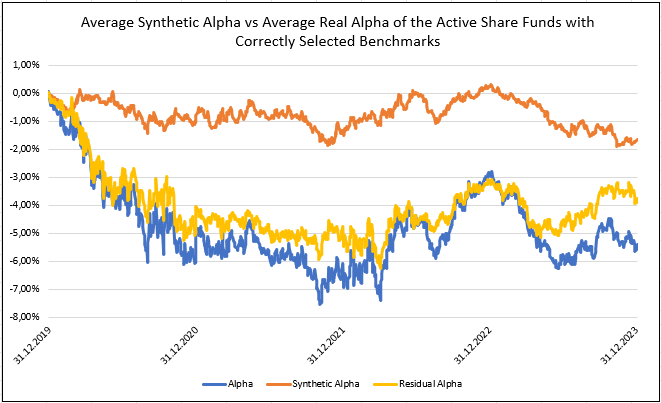

On this a part of the examine, we centered on analyzing the typical artificial alphas and common actual alphas for each teams of funds.

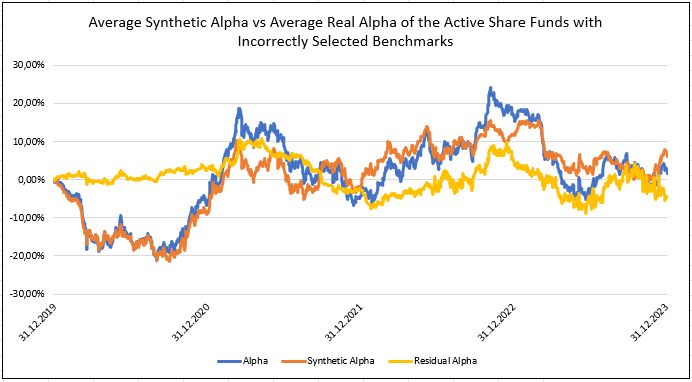

What’s the distinction between Figures 5&6? Let’s look nearer. Determine 5 depicts the typical Alpha, Artificial Alpha and Residual Alpha of funds which have a excessive Energetic Share measure, however they picked their benchmark incorrectly – one other benchmark can be ample as their portfolio is just not composed of S&P 500 shares (or large-cap shares) in any respect and, for instance, are shopping for lots of small/mid caps, or worth shares. Determine 5 reveals that the abstract alpha of these funds is roughly 0%, and many of the variation might be defined by systematic components (the blue line, Alpha, could be very near the orange line, Artificial Alpha). Idiosyncratic bets have a small influence on the funds’ efficiency. Funds could rating excessive on the Energetic Share measure, however managers’ exercise interprets into systematic issue bets, and from the buyers’ perspective, it may be simpler and cheaper simply to purchase the ETF with the required issue publicity (small worth, for instance).

Determine 6 depicts the typical Alpha, Artificial Alpha, and Residual Alpha of funds which have the excessive Energetic Share measure, and so they picked the right benchmark – many of the funds’ bets are from the S&P 500 universe (or large-cap shares basically). Managers of funds attempt to file overperformance in opposition to the benchmark by weighting shares otherwise however utilizing the identical funding universe because the benchmark-like S&P 500 funding universe. We are able to see that it is a onerous process to do, as, on common, the Alpha of those funds is destructive. However on the optimistic aspect, their Artificial Alpha is near 0%, in order a bunch, they don’t run any systematic issue bets (aside from their publicity to giant caps), and all the Alpha might be defined by the idiosyncratic (particular person) bets of managers, which selective choose their favourite shares from the S&P 500 universe, obese them and attempt to beat the benchmark. It’s a tough job to do, however a minimum of right here, the Energetic Share really measures stock-picking exercise.

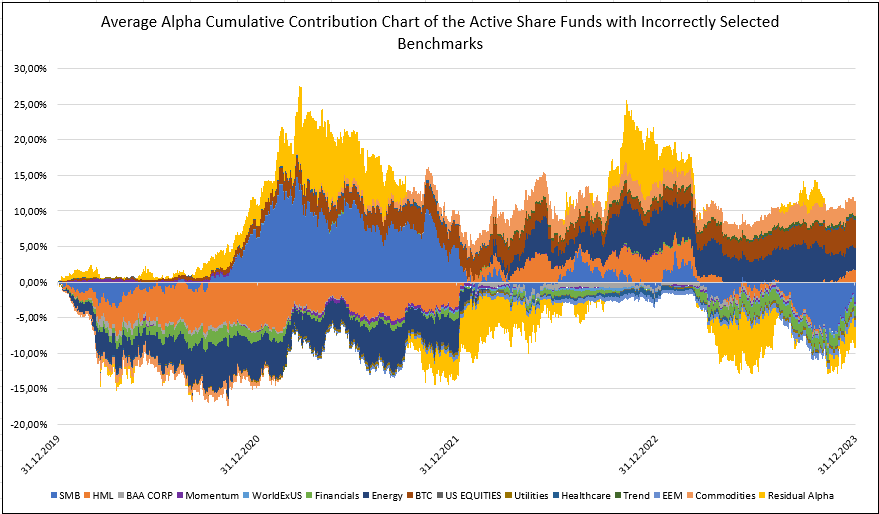

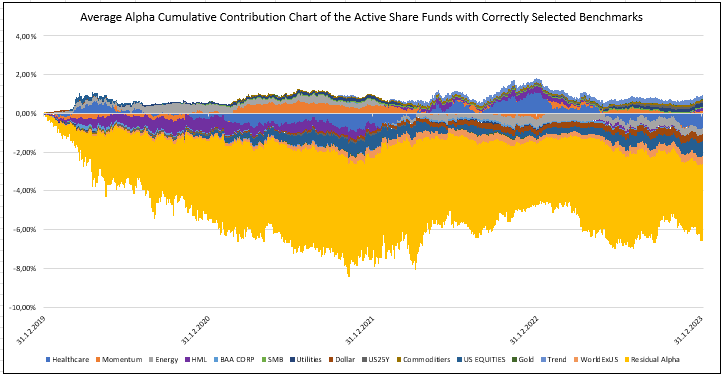

As soon as once more, listed below are the Alpha decomposition charts, and we are able to see that the systematic components (worth/development, small/large, momentum, and sector bets) have a profound influence on the primary group of funds (Determine 7). However, within the second group (Determine 8), many of the alpha comes from inventory selecting (yellow space—residual alpha).

Conclusion

So, what’s our conclusion? The connection between Energetic Share measure and alpha is extra complicated than it might appear on the first look. Managers typically select benchmarks that aren’t solely correct, which ends up in skewed info from Energetic Share. On this case, the managers over/underperformance is normally pushed by systematic components (giant/small, worth/development, momentum, and/or sector components) and never by particular person stock-picking talent. Between managers, that choose correct benchmarks for his or her funds, the alpha is pushed by stock-picking talent but it surely additionally doesn’t imply that prime energetic share ought to routinely translate into the fund’s outperformance. Subsequently, in one of the best case, the insights gained from Energetic Share are extremely distorted. To realize extra significant insights right into a supervisor’s efficiency and their relative over/underperformance in comparison with a benchmark, it’s more practical to conduct an element evaluation of the alpha moderately than relying solely on the easy measure of Energetic Share.

Writer: Sona Beluska, Junior Quant Analyst, Quantpedia

Are you on the lookout for extra methods to examine? Go to our Weblog or Screener.

Do you wish to be taught extra about Quantpedia Professional service? Examine its description, watch movies, evaluation reporting capabilities and go to our pricing provide.

Do you wish to know extra about us? Examine how Quantpedia works and our mission.

Are you on the lookout for historic information or backtesting platforms? Examine our record of Algo Buying and selling Reductions.

Or observe us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookCheck with a buddy